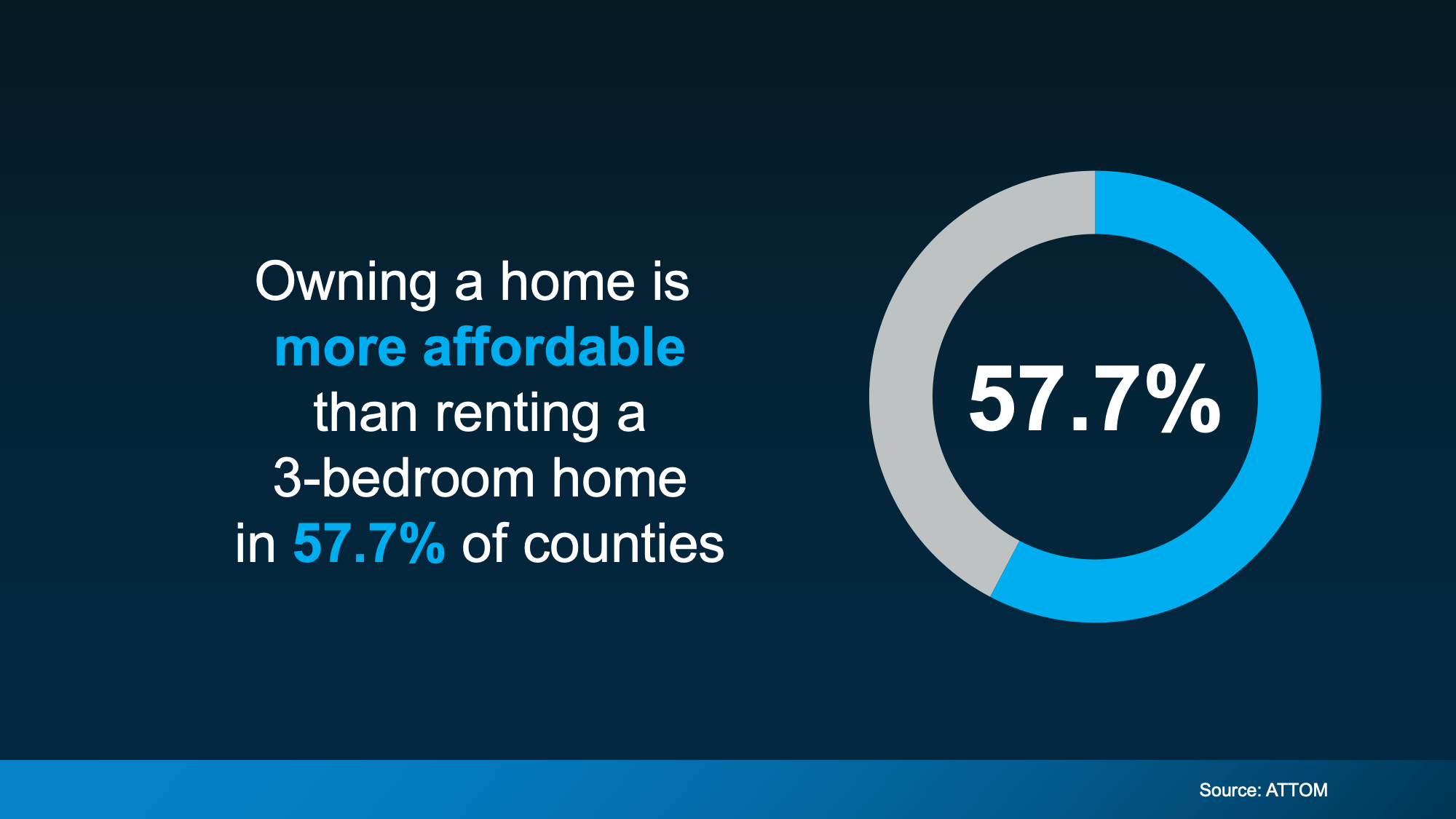

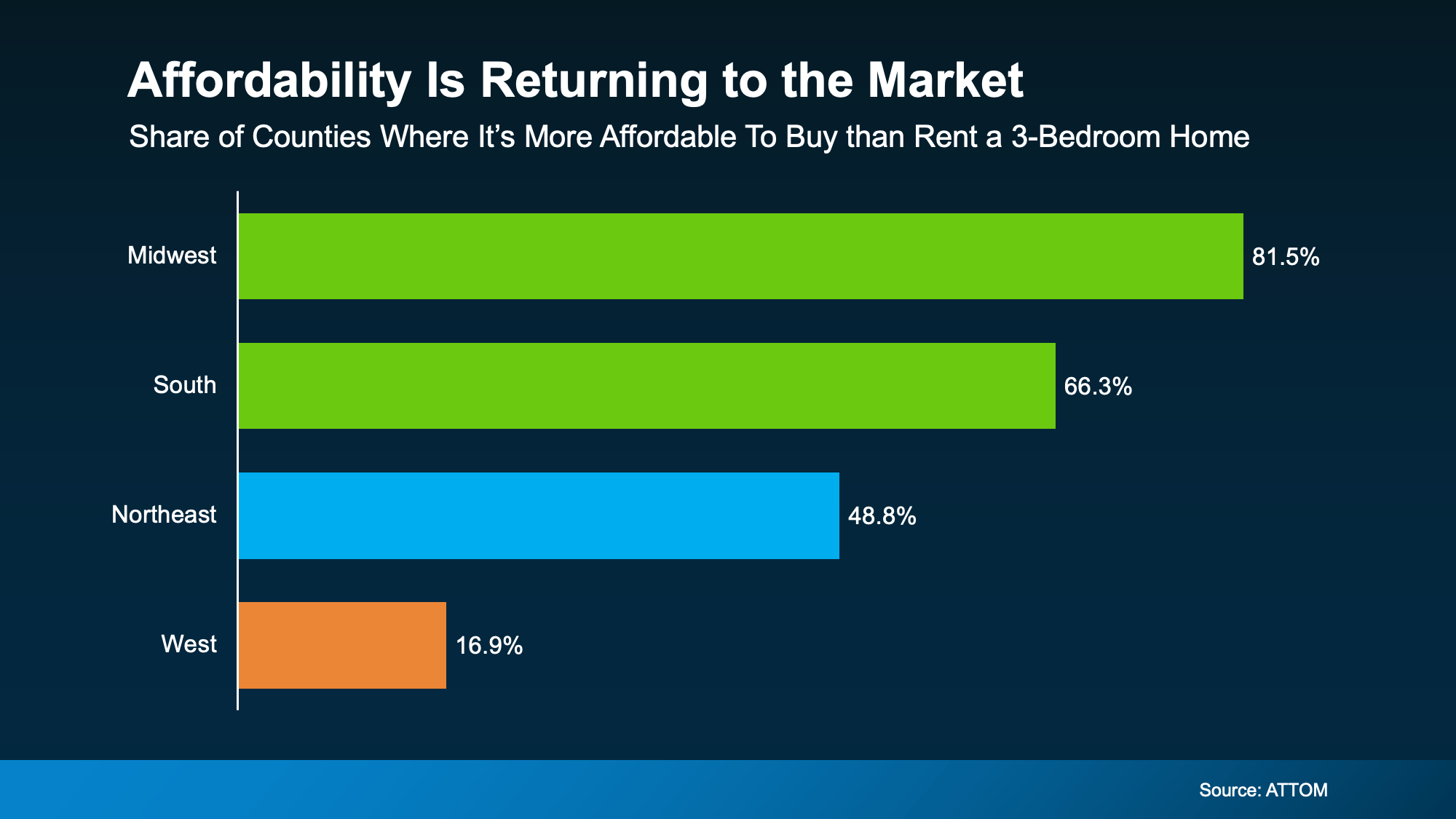

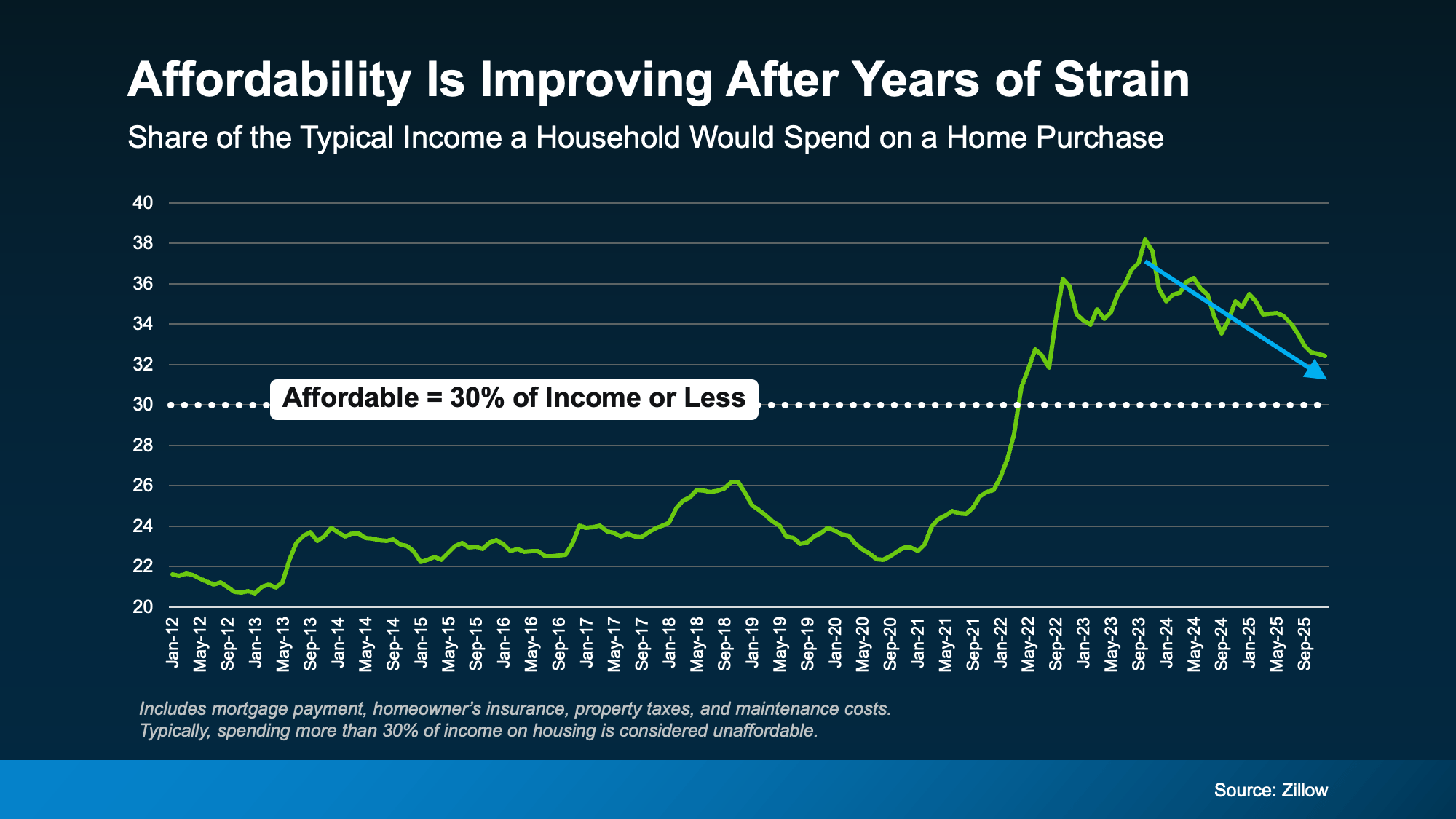

Affordability Has Improved in All 50 States.

For the past few years, affordability has been what’s stopped a lot of buyers in their tracks. Maybe it stopped you, too.

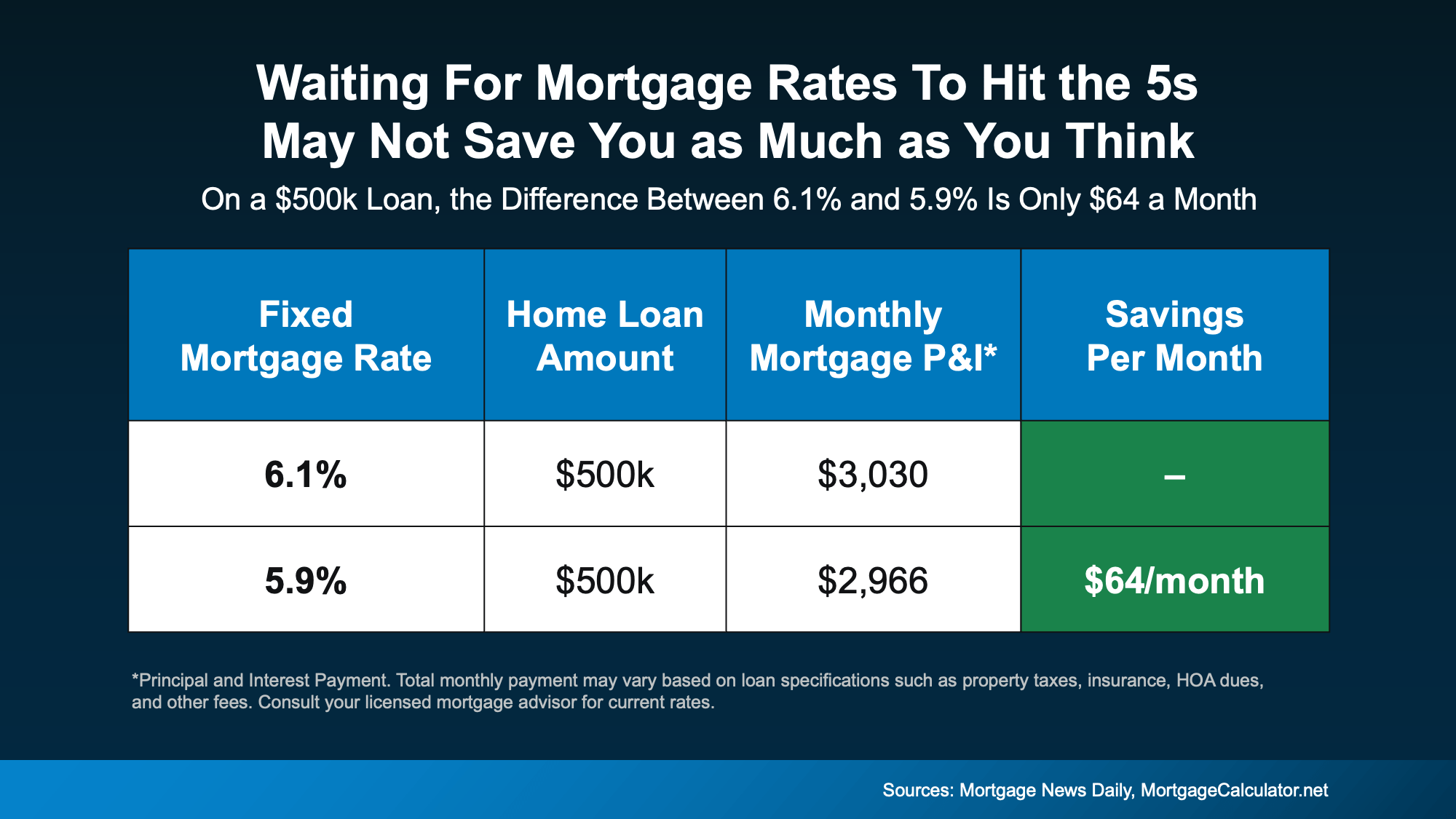

At some point you probably did the math, looked at the monthly payment, and decided to pause your search and wait for things to get better. But here’s something you may have missed while you’ve been sitting on the sidelines.

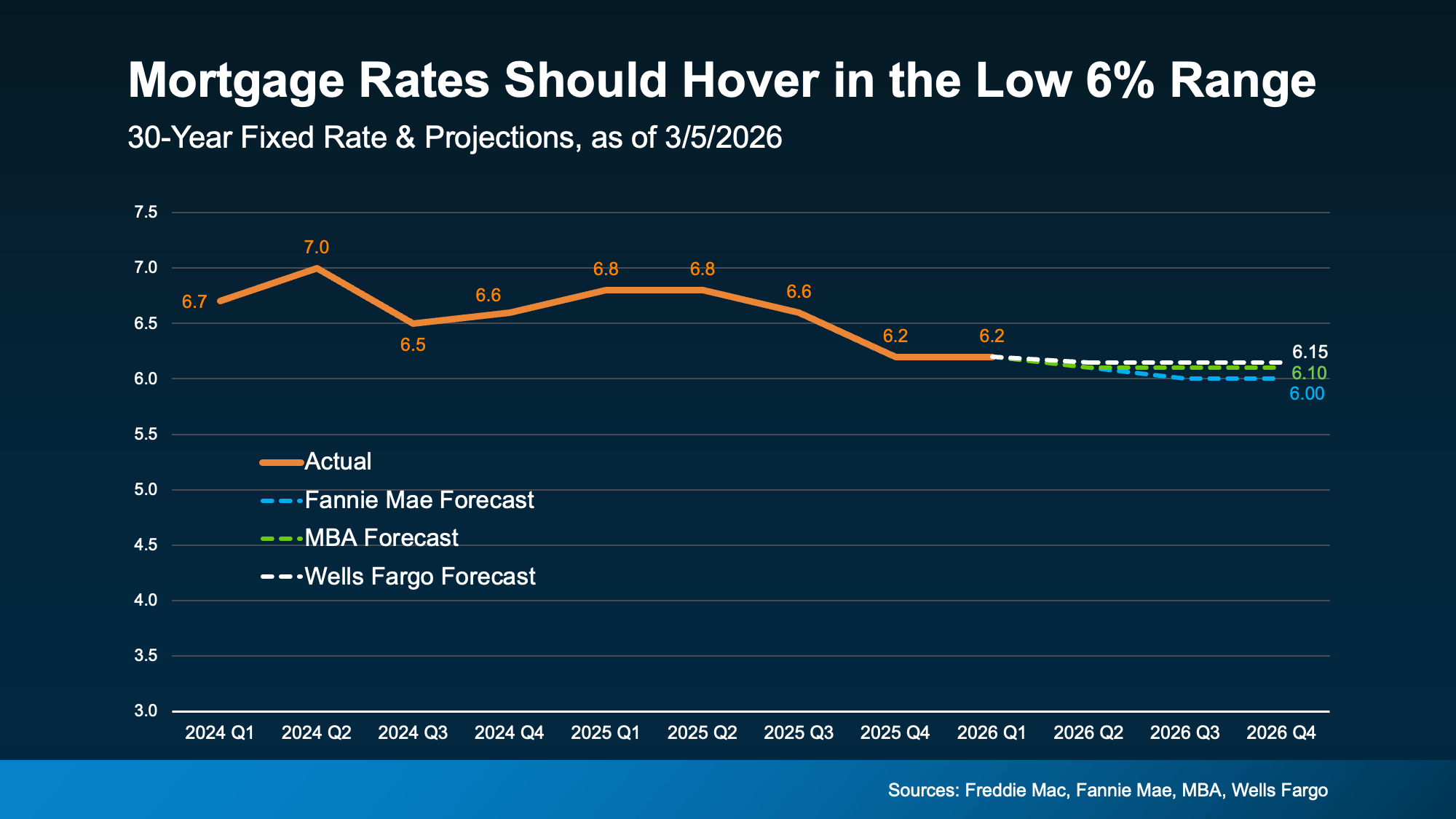

Over the last year, housing affordability has improved in all 50 states. Yes, you read that right. It’s gotten better in every single state.

That’s based on new research coming out of First American. And while housing is still fairly expensive compared to historical standards, the pressure buyers felt over the last few years is finally starting to ease.

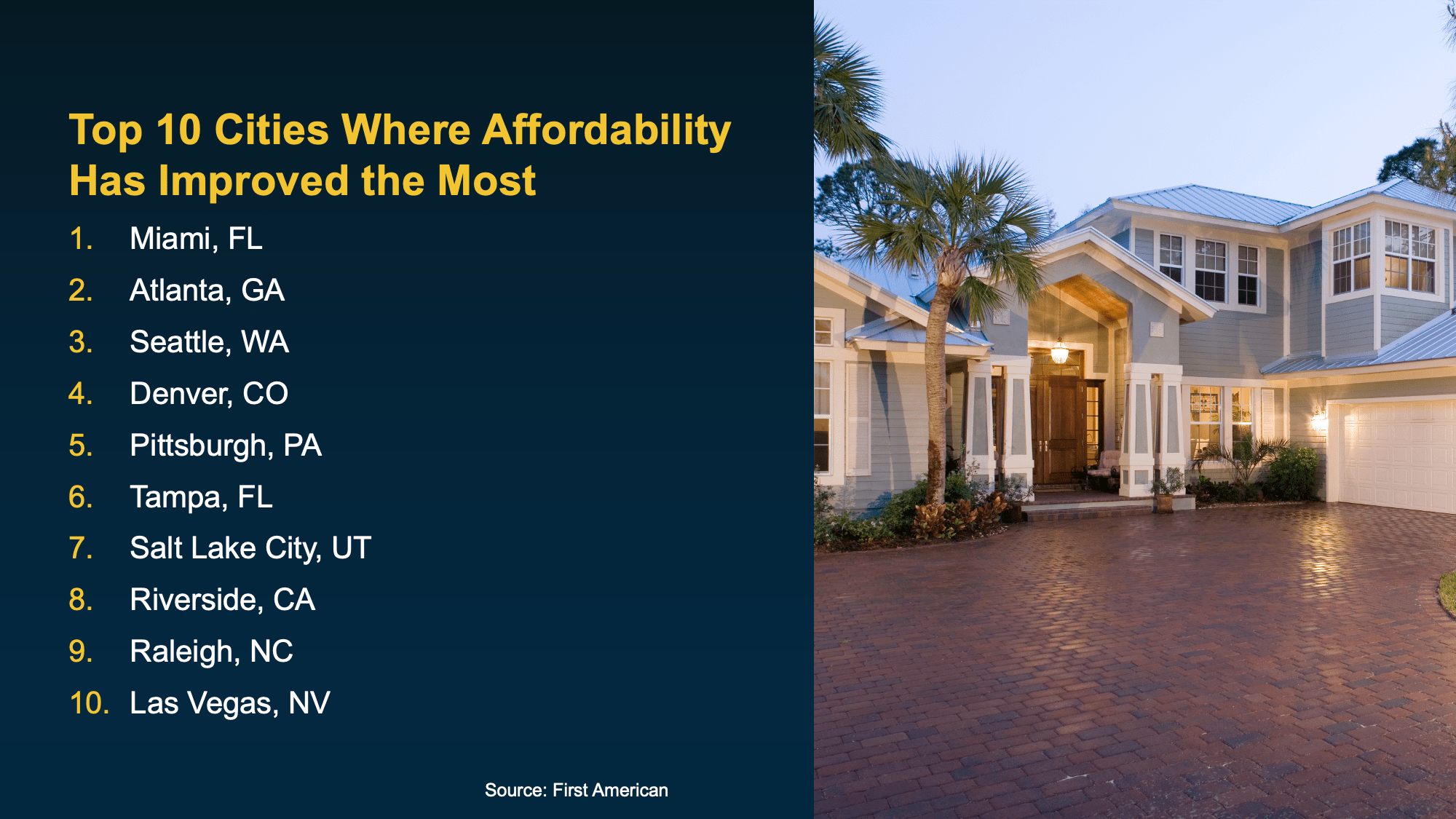

Some Areas Are Seeing Bigger Improvements

The first thing you need to know is that this isn’t just happening in one region or in a small handful of cities. The trend is happening almost everywhere.

Sure, individual states, cities, and even neighborhoods are going to vary – sometimes by a lot. But overall, more buyers are able to buy again. And in 48 of the top 50 metros, affordability has improved over the past year.

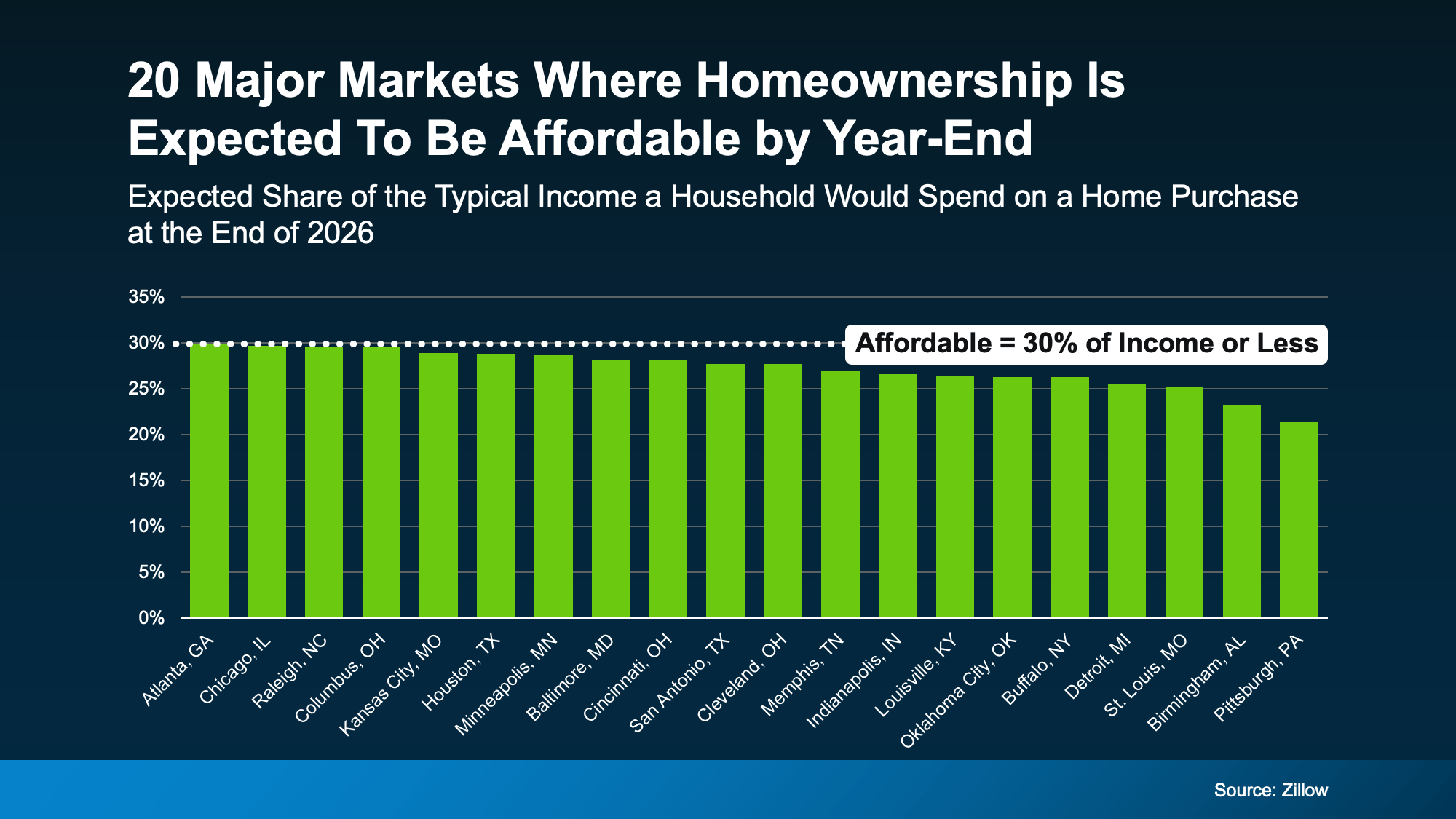

That same research breaks down which cities are seeing the biggest gains:

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

Just in case you’re wondering: why these areas? It’s simple. In many cases, it comes down to the number of homes for sale.

When buyers have more choices, it creates a healthier balance in the market and that can help bring affordability back within reach. With homes up for grabs, it opens the door a bit wider for buyers to negotiate with sellers for credits, price cuts, and more. And it gives you more chances to find a house that works for your needs and budget.

It may make more of a difference than you think.

None of this means affordability challenges have completely disappeared. Buying a home is still a big financial decision. But the trend is moving in a direction many buyers have been waiting for.

As Chen Zhao, Head of Economic Research at Redfin, puts it:

“The housing affordability crisis is showing signs of easing . . . opening the door for more Americans to make the jump to homeownership.”

Bottom Line

If you were holding off on buying, this could be exactly the signal you’ve been waiting so long for. To find out how much affordability’s improved in your area, connect with a local real estate agent.